News

McCormick Hired as New Deputy CAO of the Municipality of Cumberland

- Details

The Municipality of Cumberland has hired Allie McCormick as its new deputy chief administrative officer.

She begins her new duties with the municipality on July 13, 2026. She replaces Peter McCracken, who is becoming the new chief administrative officer upon the retirement of present CAO Greg Herrett.

“I am honoured to be part of a team that is so dedicated to serving its residents and communities,” McCormick said. “Throughout my career, I have been passionate about local government and the important role it plays in people's everyday lives.

“I look forward to working with council, staff, community partners and residents to support the municipality's goals and help build on the many successes already taking place across Cumberland County."

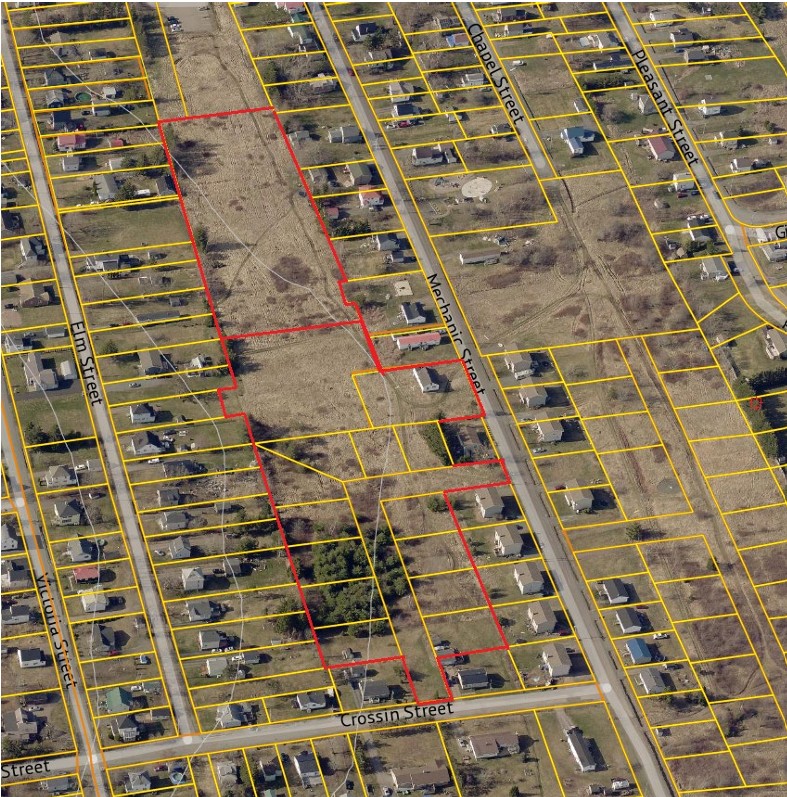

Work Beginning on New Springhill Housing Project

- Details

Shaw Rural Housing, in cooperation with the Nova Scotia Co-operative Council, is set to begin the latest project to improve the housing supply in Springhill and area.

Work is expected to begin early the week of June 15 on a new housing development that will eventually see a mixture of single-unit dwellings, duplexes, triplexes and fourplexes. The first four buildings in the initial phase will be multi-unit buildings with 21 units in total.

Job Posting: Director of Recreation

- Details

The Municipality of the County of Cumberland is currently accepting resumes for a Director of Recreation.

Springhill and River Hebert remember their communities’ coal mining heritage

- Details

It will be 70 years ago on Nov. 1 when runaway coal cars sparked coal dust in the Number 4 mine under Springhill, causing an explosion that killed 39 people on the surface and underground in what would be the second of three major disasters in the community’s history.

Clyde Jones said his father, Bill, was working on the surface that afternoon after trading shifts with a friend who wanted to go deer hunting. He was working on the tipple, where loaded coal cars were dumped after reaching the surface.

Just after 5 p.m. coal cars detached from the others and hurtled down the mine shaft, striking a power cable. Arching electricity sparked suspended coal dust and the resulting explosion blew through the mine and to the surface.

His father was blown clear, landing several yards from the shaft. He was burned badly and died six days later in hospital.

Jones was the guest speaker at Springhill’s annual Miners’ Memorial Day commemoration at St. Andrew’s Wesley United Church on June 11, 2026.

He said Springhill has a story to tell – one of perseverance – and it’s important for today’s generation and those that follow to continue telling the story of a community that has continued to overcome over the years.

“Stories are how we honour those who came before us. Each person and each family has a story worth preserving for future generations,” he said. “In my own life, many of these stories were not firsthand. They happened long before I was born, but they the still shaped me and the man I am today.

“Here in our town, we have lost so many lives to mining over the years. And yet, Springhill has always shown resilience. Time and time again our community has found the strength to stand back up and continue searching for a better life.”

Job Posting: Tourism Ambassador Summer Term

- Details

The Municipality of the County of Cumberland is currently accepting resumes for a Tourism Ambassador summer term.